January 30, 2026, marks a watershed moment in the annals of India's financial technology landscape. The Reserve Bank of India has taken a decisive step that promises to fundamentally reshape the architecture of digital payments in the country. In a move designed to democratize financial access, the RBI Governor officially announced the comprehensive expansion of the offline e-Rupee (e₹) service specifically targeted at feature phone users. This is not merely an incremental update but a paradigm shift aimed at bridging the stark digital divide that still separates metropolitan India from its rural hinterlands. The initiative seeks to bring the benefits of the Central Bank Digital Currency (CBDC) to the last mile, ensuring that lack of internet connectivity or expensive hardware is no longer a barrier to participation in the formal digital economy.

For years, while the Unified Payments Interface (UPI) has been the poster child of India's fintech success story globally, a significant demographic remained on the periphery. The reliance on smartphones and stable high-speed internet data meant that millions of users with basic mobile phones were excluded from the digital revolution. The RBI's latest directive addresses this exclusion head-on. By enabling offline transactions on basic handsets, the central bank is effectively declaring that financial inclusion should not be held hostage by the type of device a citizen owns. This move is expected to unlock the digital potential of a vast user base that has traditionally relied solely on cash.

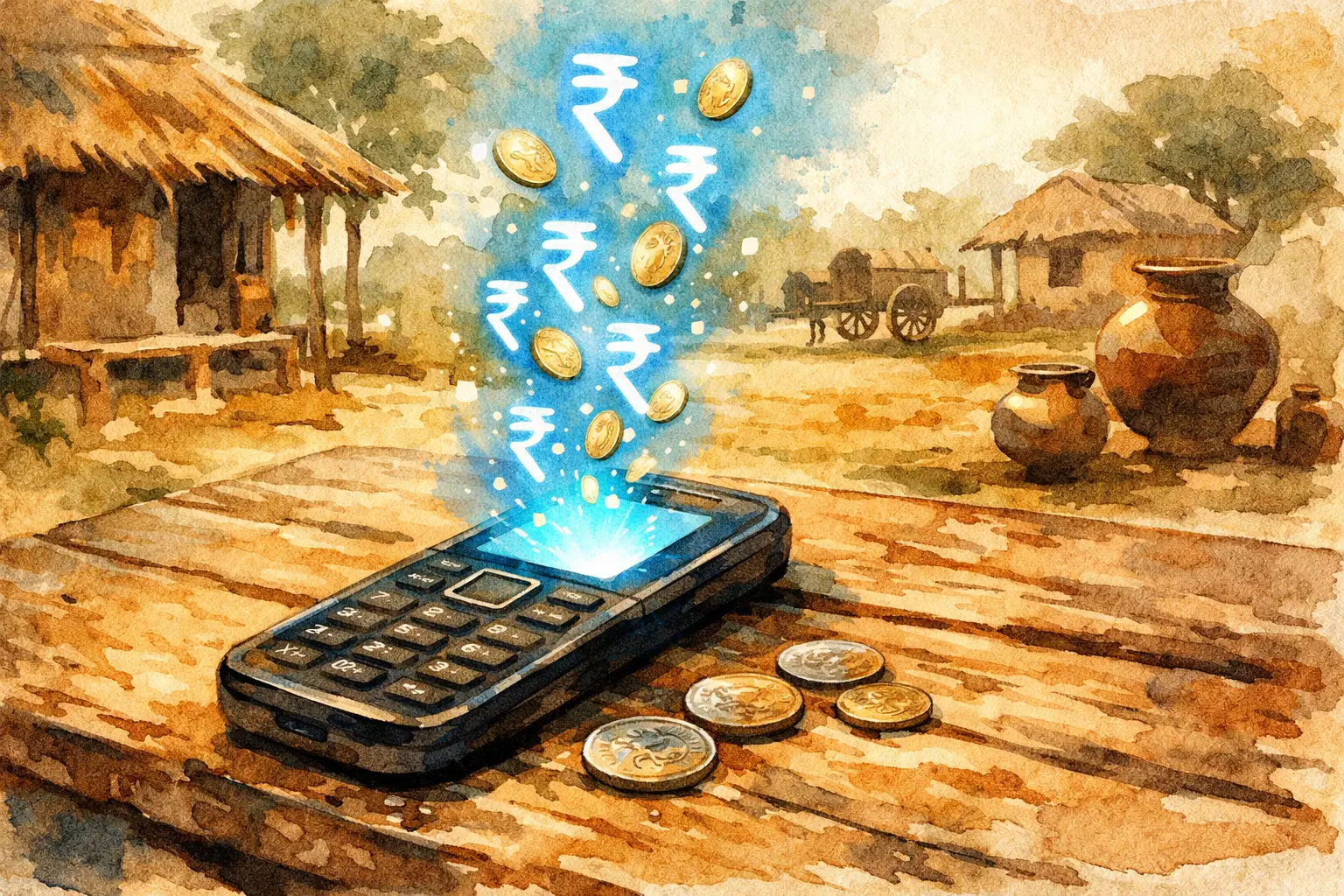

The technical backbone of this new system relies heavily on USSD (Unstructured Supplementary Service Data) protocols. This technology is familiar to anyone who has used a mobile phone in the pre-smartphone era to check prepaid balances. By dialing a simple short code, users can access a menu-driven interface that allows them to transfer funds, check balances, and review transaction history. The genius of this approach lies in its simplicity. It strips away the complex, graphical user interfaces of modern apps and replaces them with a text-based system that functions reliably even on the most basic network signals. This ensures that a farmer in a remote village can execute a transaction with the same finality as a tech professional in a metro city.

Perhaps the most empathetic feature of this rollout is the integration of voice-based payment capabilities. Recognizing that literacy—both digital and traditional—remains a hurdle for many, the RBI has pushed for an Interactive Voice Response (IVR) system. This allows users to conduct transactions through voice commands in their native languages. By removing the need to type or navigate text menus, the system lowers the cognitive load on the user, making digital payments as natural as a verbal conversation. This feature alone has the potential to onboard millions of senior citizens and semi-literate users who find typing on a keypad daunting.

In his press briefing in Mumbai, the RBI Governor also highlighted the introduction of Near Field Communication (NFC) based solutions for offline payments. This is particularly crucial for areas with intermittent or zero network coverage, such as deep forest settlements or remote hill stations. The proposed system envisions the use of offline wallets or cards that can communicate with a merchant's device without hitting a bank server in real-time. This essentially mimics the physical exchange of cash but in a digital format. For street vendors and small merchants operating in connectivity-shadow zones, this ensures that business does not stop when the network is down.

From a macroeconomic perspective, this initiative is a strategic move to reduce the economy's heavy dependence on physical currency. The logistical cost of printing, securing, transporting, and managing the lifecycle of paper currency is immense. By encouraging the adoption of the e-Rupee in the cash-heavy rural economy, the central bank aims to significantly trim these operational costs. Furthermore, it addresses perennial issues associated with physical cash, such as the circulation of soiled notes and the shortage of small change, which often hampers micro-transactions in daily commerce.

Security remains a paramount concern in any digital financial system, and the RBI has assured that the offline e-Rupee is built on robust encryption standards. Even though the transactions occur offline, the digital tokens are cryptographically secured on the device or card. Mechanisms are in place to prevent double-spending and to recover funds in case of device loss or theft. By maintaining a ledger that syncs when connectivity is eventually restored, the system balances the convenience of offline usage with the integrity required of a central bank currency.

The RBI has set an ambitious target to double the daily volume of digital rupee transactions in the fiscal year 2026. To achieve this, a massive outreach program is being mobilized involving banks, fintech intermediaries, and local community leaders. The focus is not just on infrastructure but on behavioral change. Camps and demonstrations in villages will be crucial to demystify the technology and build trust among a population that has historically viewed cash as the only reliable store of value.

It is important to distinguish this offering from the existing UPI framework to understand its unique value proposition. UPI is fundamentally an inter-bank transfer system that requires real-time communication with banking servers. If a bank's server is down, the transaction fails. The e-Rupee, however, is a direct liability of the central bank and functions like digital cash held in a wallet. The offline capability means that it is immune to the server outages that occasionally plague the banking system, offering a level of reliability that is essential for daily essential transactions.

This development is poised to revolutionize micro-transactions across the country. Consider the ecosystem of vegetable sellers, tea stall owners, and bus conductors where speed and small denominations are key. The offline e-Rupee allows for quick settlements without the friction of finding change or waiting for a payment confirmation wheel to stop spinning on a slow network. It increases the velocity of money in the informal sector, which is the engine of India's rural economy.

However, the path to widespread adoption is paved with challenges. Overcoming the inertia of cash habits is the biggest hurdle. Trust is hard-earned and easily lost in the financial sector. The RBI and its partners must ensure that the user experience is flawless and that grievance redressal mechanisms are accessible and responsive. Education will play a pivotal role here; users need to understand that this 'invisible money' is as safe and valid as the paper notes they keep in their chests.

In conclusion, the expansion of the offline e-Rupee on January 30, 2026, is a defining step towards a truly inclusive digital India. It acknowledges the reality that while India is a global tech hub, it is also home to millions who are yet to touch a smartphone. By tailoring technology to fit the needs of the feature phone user, the RBI is ensuring that the digital dividend is distributed equitably. If successful, this initiative will not only modernize the rural economy but also serve as a global case study for financial inclusion in developing nations.

No Comment Yet.

Stay informed with breaking news, trending stories, and in-depth analysis.